Xaar’s 2025 Results Reinforce the Speed of Adoption in Inkjet

Earlier this morning, (March 24) Xaar reported its Full Year 2025 results, and there are some strong signals coming through - particularly around the continued momentum in printhead technology for industrial applications.

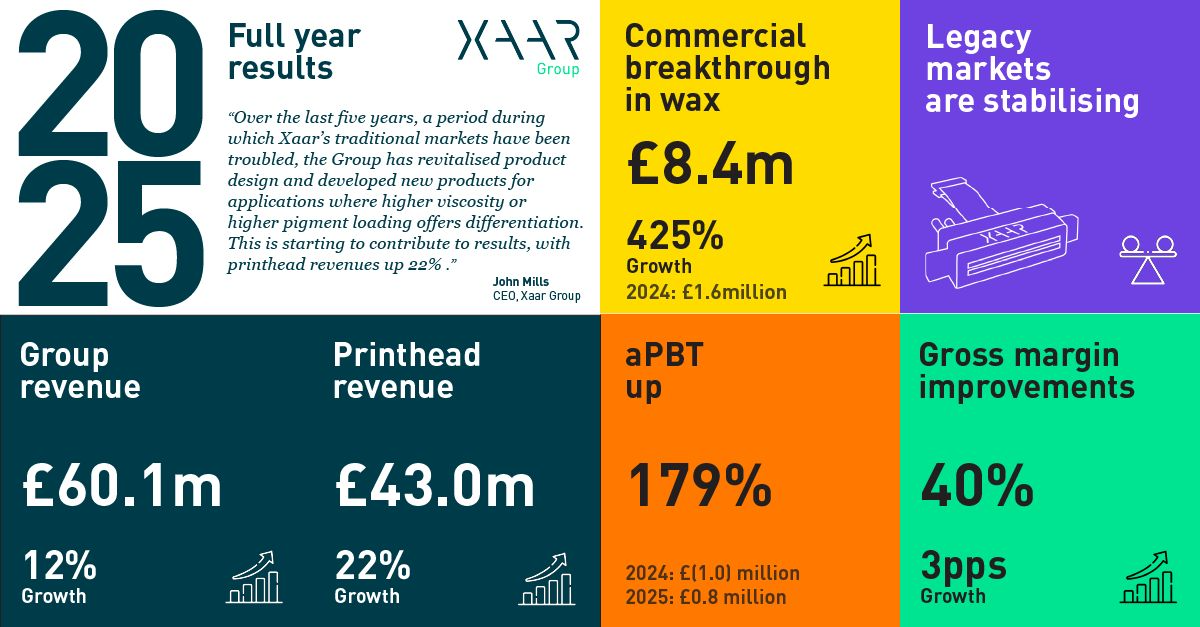

The standout headline is 22% revenue growth in the Printhead division, with printhead revenues themselves up 27%. That’s not incremental progress - that’s meaningful acceleration, and it points to real traction in key industrial application areas.

According to Xaar, a big driver behind this recent progress is the jewellery 3D wax market. It’s a compelling example of how quickly ultra high viscosity inkjet technology can penetrate and scale within a new vertical when the application fit is right. It reinforces a broader point we’re seeing across industrial print - when the technology aligns with a clear production need, adoption can move fast.

Stepping back, the bigger picture here is one of increasing visibility. The scale and clarity of Xaar’s medium-term opportunity continues to build, and these results suggest the business is converting that potential into tangible performance.

Commenting on the performance and outlook, John Mills, Chief Executive, said:

"Xaar's differentiated technology can deposit precise volumes of high viscosity inks with pin-point accuracy. This capability brings benefits, increasingly in new applications which are driven by global trends towards digital manufacturing and the need to reduce process waste. Over the last five years, a period during which Xaar's traditional markets have been troubled, the Group has revitalised product design and developed new products for applications where higher viscosity or higher pigment loading offers differentiation. This is starting to contribute to results, with printhead revenues up 22% in 2025. Commercial breakthrough has been achieved this year in wax 3D printing, and demonstrable progress is being made in several other new applications.

Operationally in 2025 the focus has been on margin enhancement, including opening a facility in Dongguan to be closer to Asian customers and to provide better supply chain resilience and efficiency.

The timing of revenue from new applications, which generally require several layers of customer qualification, can be uncertain. This complexity, while sometimes challenging, eventually leads to much clearer competitive advantage, along with a valuable annuity revenue for printheads. Early trading in 2026 is in line with expectations. The order book is healthy for this time of year, and the Board believes the Group is well positioned for further progress - both in 2026 and in the longer term."